Introduction

TDS compliance is not a one-size-fits-all solution. Different industries, such as manufacturing, media, and technology, face unique challenges when dealing with foreign remittances. This blog dives into real-world case studies, uses figures to provide clarity, and offers practical steps to ensure smooth compliance while avoiding tax disputes.

Key TDS Challenges by Industry

1. Manufacturing: Licensing of Proprietary Designs

Manufacturers often pay royalties to foreign entities for using proprietary designs, patents, or trademarks. These payments typically fall under Section 9(1)(vi) as royalties.

- Scenario:

- XYZ Ltd., an Indian automobile company, pays ₹50,00,000 to a German firm for licensing a patented engine design.

- Analysis:

- Outcome:

- TDS = ₹50,00,000 × 10% = ₹5,00,000.

- XYZ Ltd. must deduct TDS under Section 195 and file Form 15CA/15CB.

2. Media: Content Licensing and Broadcasting Rights

The media industry frequently licenses digital media or broadcasting rights from foreign entities. These payments are generally classified as royalty if they involve copyrighted material.

- Scenario:

- ABC Media Pvt. Ltd. pays ₹1,00,00,000 to a US-based company for broadcasting rights to a Hollywood movie.

- Analysis:

- Payment qualifies as royalty under Section 9(1)(vi) since it involves copyrighted content.

- DTAA Implication: Under the India-USA DTAA, TDS applies at 10%.

- Outcome:

- TDS = ₹1,00,00,000 × 10% = ₹10,00,000.

- ABC Media Pvt. Ltd. must ensure compliance with Form 15CA/15CB.

- Case Reference:

- DIT v. New Skies Satellites BV (2016): Payments for broadcasting rights were held taxable as royalty under Section 9(1)(vi).

3. Technology: Royalty vs. Operational Payments

The technology industry faces challenges in classifying payments for SaaS, cloud services, and software licenses as royalty, fees for technical services (FTS), or operational expenses.

- Scenario 1:

- DEF Tech Pvt. Ltd. pays ₹25,00,000 to AWS (US) for cloud storage services.

- Analysis:

- Payment for shared cloud storage does not involve IP transfer or technical knowledge and is treated as an operational expense.

- Outcome:

- No TDS is required, but Form 15CA (Part D) must be filed.

- Scenario 2:

- DEF Tech Pvt. Ltd. pays ₹50,00,000 to a US company for a customized SaaS solution with knowledge transfer.

- Analysis:

- Payment qualifies as FTS since the service “makes available” technical expertise.

- DTAA Implication: Under the India-USA DTAA, TDS applies at 10%.

- Outcome:

- TDS = ₹50,00,000 × 10% = ₹5,00,000.

- Case Reference:

- Engineering Analysis (2021): Payments for off-the-shelf software without IP transfer are not royalties.

Practical Steps for TDS Compliance Across Industries

Step 1: Classify the Payment

- Manufacturing: Determine if the payment involves royalties for patents, designs, or trademarks.

- Media: Verify if the payment involves copyrighted material or broadcasting rights.

- Technology: Identify if the payment involves:

- IP transfer (royalty),

- Technical knowledge (FTS), or

- Operational services (non-taxable).

Step 2: Check DTAA Provisions

- Evaluate DTAA benefits for reduced tax rates or exemptions.

- Apply the “make available” clause for FTS taxation.

- Obtain a Tax Residency Certificate (TRC) and Form 10F from the foreign entity.

Step 3: Deduct TDS

- Apply the lower of the domestic tax rate or DTAA rate.

- Common rates:

- Royalty: 10%-15%.

- FTS: 10% under India-USA/UK DTAAs.

- Common rates:

Step 4: File Compliance Forms

- File Form 15CA/15CB for all foreign remittances.

- Maintain documentation like agreements, invoices, and TRCs.

Taxability Matrix for Key Industries

| Industry | Payment Type | Taxable? | Reason |

| Manufacturing | License for patented designs | Yes (Royalty) | IP use qualifies as royalty under Section 9(1)(vi). |

| Media | Content licensing | Yes (Royalty) | Payments involve copyrighted content. |

| Technology | SaaS for CRM | No | Operational expense, no IP or technical knowledge. |

| Technology | Customized SaaS with knowledge transfer | Yes (FTS) | “Makes available” technical expertise. |

Case Study: Real-World Application

Facts:

- MNO Ltd., an Indian company, engages in three transactions:

- Pays ₹40,00,000 to a UK firm for using a proprietary product design.

- Pays ₹20,00,000 to a US company for licensing a documentary.

- Pays ₹30,00,000 to AWS for cloud storage.

Analysis:

- Proprietary Product Design:

- Payment qualifies as royalty under Section 9(1)(vi).

- TDS = ₹40,00,000 × 10% (India-UK DTAA) = ₹4,00,000.

- Content Licensing:

- Payment qualifies as royalty under Section 9(1)(vi).

- TDS = ₹20,00,000 × 10% (India-USA DTAA) = ₹2,00,000.

- Cloud Storage:

- Payment is an operational expense.

- No TDS required, but Form 15CA (Part D) must be filed.

Value Addition: Best Practices for TDS Compliance

1. Maintain Robust Documentation

- Clearly define the payment type in agreements (e.g., royalty, FTS).

- Retain TRCs, invoices, and remittance proofs.

2. Avoid Common Pitfalls

- Misclassification of payments (e.g., operational expenses as royalty).

- Non-compliance with DTAA documentation requirements (e.g., TRC, Form 10F).

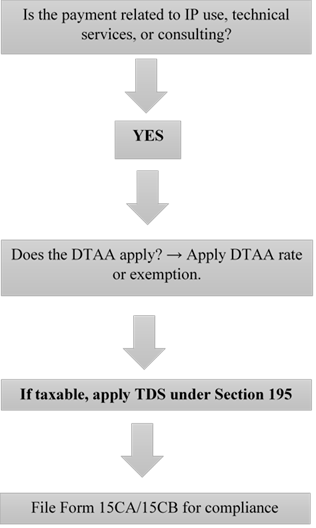

3. Leverage Flowcharts for Payment Classification

Q&A: Addressing Reader Queries

- Are SaaS payments always taxable?

- No. SaaS payments are taxable as FTS only if they “make available” technical expertise. Shared services without IP transfer are non-taxable.

- What is the TDS rate for royalties under DTAA?

- Most DTAAs (e.g., India-USA) cap royalty TDS at 10%.

- Do cloud storage services require TDS deduction?

- No, if classified as operational expenses with no IP transfer.

- How do I ensure DTAA benefits?

- Obtain a TRC and file Form 10F.

Conclusion

Navigating TDS compliance across industries requires understanding payment classifications, leveraging DTAA benefits, and ensuring robust documentation. From royalty payments in manufacturing to cloud services in technology, accurate tax compliance safeguards businesses from disputes and penalties.

Need expert guidance on TDS compliance? Connect with us for tailored solutions and ensure seamless compliance for your business!