In today’s globalized economy, companies frequently engage non-resident consultants for services ranging from IT advisory to legal opinions. While such arrangements boost operational efficiency, they also trigger TDS liability under Indian tax law, particularly under Section 195 of the Income-tax Act, 1961. This blog simplifies the taxability of cross-border consulting payments, with practical case studies, relatable scenarios, and compliance tips.

Key Determinants of Taxability

- Business Connection and Permanent Establishment (PE)

- Payments to non-residents are taxable in India if:

- A Non-resident individual or entity has a business connection in India (Section 9).

- A Permanent Establishment (PE) is created, as defined in the applicable Double Taxation Avoidance Agreement (DTAA).

- “Make Available” Clause

- Many DTAAs limit the taxation of Fees for Technical Services (FTS) to instances where:

- The service imparts technical knowledge, experience, or skill to the payer.

- The payer can independently use this knowledge without further assistance.

- Nature of Services

- Payments for managerial, technical, or consultancy services are classified as FTS under Section 9(1)(vii).

- Legal, IT, and business advisory services often fall into this category.

Case Laws Shaping Taxability

1. CIT v. Havells India Ltd. (208 Taxman 114)

Facts:

- Havells India Ltd. paid fees to a US-based company for witness testing and certification.

- No TDS was deducted, claiming exemption under Section 9(1)(vii)(b) as income sourced outside India.

- The Assessing Officer disallowed the expense under Section 40(a)(ia), arguing it was taxable as fees for technical services (FTS).

Issues:

- Were fees for technical services taxable in India, requiring TDS under Section 195?

Judgment:

TDS on Fees for Technical Services (In Favor of Revenue)

- The source of income was in India, as manufacturing and export activities originated in India.

- FTS was taxable in India, and TDS deduction was mandatory under Section 195.

- Disallowance under Section 40(a)(ia) was upheld as the Tribunal incorrectly treated the fees as sourced outside India.

Final Ruling: TDS on Technical Fees –TDS deduction was required, making the payment taxable in India.

Case Scenarios:

Scenario 1: Management Consulting Services

- Facts:

- ABC Ltd., an Indian company, hires a UK-based consultant for ₹25,00,000 to develop a strategic business plan.

- Analysis:

- The consultant provides periodic recommendations but does not “make available” technical knowledge.

- Under the India-UK DTAA, the “make available” clause excludes such payments from FTS taxation.

- Outcome:

- Payments are not taxable in India.

- ABC Ltd. must file Form 15CA (Part D) for remittance without TDS.

Scenario 2: IT Advisory with Knowledge Transfer

- Facts:

- XYZ Ltd. pays ₹50,00,000 to a US-based IT consultant for implementing a cloud system.

- The consultant trains XYZ’s IT team, enabling them to manage the system independently.

- Analysis:

- The service “makes available” technical expertise, qualifying as FTS.

- Under the India-USA DTAA, TDS applies at 10%.

- Outcome:

- TDS = ₹50,00,000 × 10% = ₹5,00,000.

- XYZ Ltd. must deduct TDS and file Form 15CA/15CB.

Scenario 3: Legal Opinion

- Facts:

- DEF Pvt. Ltd. pays ₹15,00,000 to a Singapore-based law firm for an opinion on Indian corporate law.

- Analysis:

- Legal advice does not involve “making available” technical knowledge.

- Payments are not taxable under the India-Singapore DTAA.

- Outcome:

- No TDS is required.

- DEF must file Form 15CA (Part D) for remittance.

Taxability Matrix for Consulting Payments

| Service Type | Taxable? | Reason |

| Business strategy consulting | No | Does not “make available” technical knowledge. |

| IT advisory with knowledge transfer | Yes (FTS) | Knowledge is “made available” to the payer. |

| Legal opinion | No | General advice, no technical expertise imparted. |

| Customized technical training | Yes (FTS) | Transfers reusable technical skills. |

Compliance Checklist

- Determine the Nature of Service:

- Classify the payment as FTS or general consulting.

- Evaluate whether the service “makes available” technical expertise.

- Check DTAA Applicability:

- Review the relevant DTAA for reduced rates or exemptions.

- Obtain a Tax Residency Certificate (TRC) and file Form 10F.

- Deduct TDS Where Applicable:

- Apply TDS at the domestic rate or DTAA rate, whichever is lower.

- Common TDS rates for FTS:

- 10% under DTAA with USA, UK, etc.

- 20% under domestic law if DTAA benefits are not claimed.

- File Forms for Foreign Remittance:

- File Form 15CA/15CB for all foreign payments, whether taxable or not.

- Maintain Documentation:

- Agreements specifying the scope of services.

- Copies of invoices and proof of remittance.

Value Addition: Practical Tips

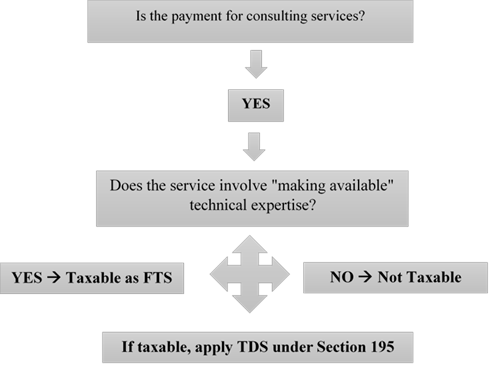

1. Flowchart for TDS on Consulting Payments

2. Common Pitfalls to Avoid

- Misclassification: Treating all consulting payments as taxable FTS.

- Ignoring DTAA Benefits: Overpaying TDS by not claiming treaty exemptions.

- Lack of Documentation: Failure to substantiate the non-taxability of payments.

Conclusion

Cross-border consulting payments require careful evaluation of taxability under Section 195 and DTAA provisions. Businesses must analyse the nature of services, the “make available” clause, and the presence of a PE to ensure compliance. By adhering to proper documentation and filing requirements, companies can avoid disputes and penalties.

For expert guidance on cross-border TDS compliance, contact us today to simplify your tax challenges and ensure error-free compliance!